The Marathoner’s Edge

What Nike’s ‘Shoe Dog’ Taught Me About the High-Stakes Race of Compounding

I just finished reading Phil Knight’s memoir, Shoe Dog, and I wanted to share what I learned about the messy reality of investing and building a business.

Warren Buffett famously endorsed the book in his 2016 shareholder letter, writing:

“The best book I read last year... Phil is a very wise, intelligent and competitive fellow who is also a gifted storyteller”.

But if you look at Nike’s early finances, most conservative investors would have run for the hills.

The story of Nike isn’t a straight line to the top, it’s a twenty-year sprint on the edge of a cliff.

It is a masterclass in what Charlie Munger calls “intelligent fanaticism”, the kind of obsession that allows a founder to do things “ordinary skilled mortals cannot”.

NOTE: More essays like this land in your inbox every week. Free to subscribe, easy to unsubscribe.

The Origin: A Thesis and a Car Trunk

The company started with a “Crazy Idea” Phil Knight had while studying at Stanford.

He wrote a research paper proposing that high-quality, low-cost Japanese running shoes could disrupt the German-dominated American market.

In 1962, he flew to Japan with no money, no company, and a fake name: Blue Ribbon Sports.

He secured distribution rights from a manufacturer called Onitsuka and started selling shoes from the trunk of his car at track meets.

For years, the company was just a middleman, but Knight was building a “signal decoder” network by talking directly to runners and coaches.

When the relationship with Onitsuka soured, Knight had to evolve or die, so he launched Nike in 1971 .

The High-Wire Act: Reinvestment at All Costs

For the first fifteen years, Nike was broke every single day.

Knight’s philosophy was simple: Grow or die.

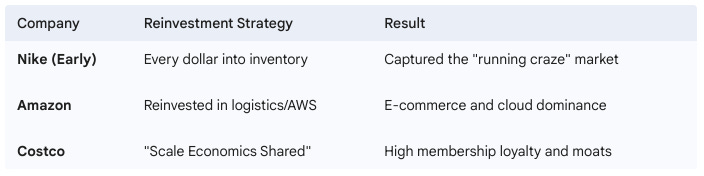

He refused to hold any cash, plowing every dollar of profit back into ordering more inventory to keep up with doubling sales.

This created what business owners call “the float”, the gap between paying your supplier and getting paid by your customer.

Because Nike was growing so fast, the business was a “cash-eating monster” that stayed roughly 90% in debt.

I see this same pattern in modern compounding giants like Amazon.

For decades, Jeff Bezos operated at razor-thin margins, reinvesting every cent into infrastructure and AWS while critics screamed about the lack of profits .

Like Knight, Bezos knew that in a winner-take-all market, market share and “mind share” matter more than a pretty balance sheet in the short term.

The Operational “Roll Cage”: Nissho Iwai

Nike only survived because Knight built what investor Pulak Prasad calls a “roll cage” i.e. a structure that allows a business to survive a crash.

When the Bank of Oregon finally got tired of Knight’s “game of chicken” and pulled his credit line, Nike was saved by a Japanese trading company called Nissho Iwai.

Nissho looked past the debt and saw the demand, they provided the “alternative funding” that allowed Nike to survive its liquidity crisis.

This is a key lesson for investors: robust businesses often find unconventional ways to stay alive when traditional systems fail them.

Growth Mechanics: The “Buttfaces” and the Waffle Iron

Nike didn’t scale through corporate consultants, it scaled through a team of misfits who called themselves “Buttfaces”.

They were runners and accountants who were “forged by early failure” and shared a common obsession with the sport.

Phil said “Don’t tell people how to do things, tell them what to do and let them surprise you with their results”.

This culture allowed for “iterative improvement,” like Bill Bowerman pouring rubber into a waffle iron to create a better sole.

Charlie Munger notes that if you find a team of fanatics with a “reasonable hand,” management really matters .

Nike also practiced “Scale Economics Shared,” a concept popularized by Nick Sleep regarding Costco .

By constantly improving the product and focusing on the athlete, Nike gave more value back to the customer, which drove more sales, which allowed for even more reinvestment.

Nike, Phil Knight and the Buttfaces (Source: Medium Post)

Investor Takeaways: The Power of Strategic Laziness

If you are analyzing modern founder-run businesses as core holdings, Shoe Dog offers three critical lessons on resilience.

1. Fanaticism is a Competitive Moat

Look for founders like Phil Knight or Jensen Huang, people who treat their company as a “calling” rather than a career.

Obsessed founders will take the “asymmetric risks” necessary to build a global icon that a professional CEO would find too scary.

2. Survival is the Ultimate Compounding Strategy

A company can be “broke” on paper and still be an incredible investment if its cash is working to build a dominant market position.

The goal is to avoid “irreparable damage” while keeping the compounding engine running at maximum speed.

3. Be “Very Lazy” with Your Winners

Pulak Prasad advocates for “Strategic Laziness”, finding high-quality businesses and then doing nothing .

If you had sold Nike in 1973 because the debt was too high, you would have missed a 50-year run of exponential growth.

The big money is not in the buying or the selling, but in the waiting.

Conclusion: Keep Going

Phil Knight’s story ends with the IPO in 1980, but the compounding hasn’t stopped since.

He proved that “business stasis is the default”, good companies tend to stay good if they never stop innovating.

Investing, like running, is a marathon where the only way to lose is to stop.

As Knight told himself during every crisis: “Just keep going. Don’t stop”.

Buffett was right; Phil Knight is a gifted storyteller, but the best part of the story is the 50-year track record of the shoes.

I’ve learned that if you find a “Shoe Dog” running a company with high ROCE and a fanatic culture, the best thing you can do is sit on your hands and watch them run.

Happy Compounding!

Cheers,

Vikas

Disclaimer: The information contained in this report is for informational and educational purposes only and does not constitute financial, investment, or legal advice. Past performance is not indicative of future results. Investors should conduct their own due diligence before making any investment decisions.